Point Frederick – Spinnaker – May 26, 2026

The darker side of investing edge.

“Edge” is a term that gets thrown around in investing a fair amount.

Think of it like the casino. On every game in the casino, the odds favor the house.

The house has an edge. It’s a structural advantage that persists over long periods of time. In Blackjack, the house edge is different from player to player and from table to table. For most players, let’s say the house has an edge of 1 to 2%. Players who use strategy can reduce this edge; card counters can reduce this edge. The house can change the payouts, or they can increase the number of decks to increase their edge by making it more difficult for players to reduce the house’s built-in advantage.

There will be periods in which the house is a net loser. The cards just don’t flop their way. But over a long enough period, the house advantage will pay off.

The same is true for investors. Good investors have edge. There are different types of edge.

Some investors are really good at getting information or they can get it faster than others. Being an investor in public markets who obeys the law is like being a detective. It’s like putting together a jigsaw puzzle where there is a constant parallel game in which you have to hunt for the pieces. Some people are really good at finding the pieces of the puzzle faster than others.

Other investors are really good at putting together the puzzle pieces once they get them and figuring out what the picture is supposed to be before anyone else, say because they can see patterns and shapes when there are fewer puzzle pieces in place.

One key source of edge is self-possession. If you can, like Kipling’s poem If describes, keep your head when others are losing theirs, then you will outperform over time. When it’s 2009 and Citibank common is trading at $1 a share and you can have the presence of mind to load the boat while everyone else is trying to get cute with a fourway strategy involving the preferreds and options, then you can make a boatload of money. There were people who did this. David Tepper did this. It was around this time that his acolytes presented him with a trophy of male genitalia described by some as “grotesquely veiny.” I believe these sit on his desk.

Some people are just great, intuitive investors. They can recognize patterns. They have studied markets and economics for decades. They have learned what the great investors do. Others are highly talented at ready sentiment and seeing when it has reached extreme levels.

The ultimate edge today might be having a long-term time horizon. Everyone is so focused on the short-term and trading in and out of things that if you can find a good name and hold on to it (or, even better, pyramid into a larger and larger position over time), you can do very well. Think of people who bought Microsoft when Nadella took over or who bought and held Google from its IPO. Chris Hohn talks about a ten year holding period for companies with perfectly defensible moats.

There are periods for every type of edge when it’s easy and there are periods when it is hard. That’s just the cards, man. Most of the time, it’s back-and-forth. It’s a grind.

It’s a slippery trap to overestimate your edge when you’re making money and it’s coming easily. It’s even worse to beat yourself up when the cards are coming down against you.

What you need is the investing metacognition to know what your edge is and when it works and when it doesn’t. When it doesn’t, then sit on your hands. When it does, get aggressive but be vigilant for the turn.

I think a lot of retail investors are feeling cocky. Their edge was the tolerance for risk that tax-advantaged savings plans afforded them. They shovel money into the market every month (or front-loaded in the beginning of the year) into their 401ks and their IRAs. They have benefited from remarkable markets starting in 2009 with a boost to technology in 2011-2013.

Retail investors had an edge and it was they were passive at a time when being passive was efficient. Long/short was tough. Volatility was low (in an autocorrelated manner). We don’t even argue about the active/passive debate anymore. Passive has won completely. Because of this so much money is now passive that it is itself self-fulfilling.

This will work until it doesn’t. No edge is always right. People will start withdrawing from their retirement plans or they will be unable to contribute or interest rates will put up headwinds or something. Then we’ll have an interesting correction.

It feels like we’re closer to that moment than we have been in a very long time. Which means that it also feels like somewhere there is a contemporary version of Charles Prince arguing that we need to keep dancing while the music is playing.

That’s what this feels like to me.

Carson Block: ‘Maybe the dumb money is the smart money’

This is an interesting theory from Carson Block. One of the big source of retail flows is people maximizing contributions to their 401k plans. If AI leads to job cuts among the middle managers, there could be a significant reduction in retail flows. It would be ironic. We’ll need to see more evidence.

‘If you’d asked me before February, I’d tell you that I don’t see the end of the cycle anytime soon. Since February, though, I do feel differently. I’ve done a 180 on AI. I think AI is going to displace a significant number of knowledge worker jobs. It’s going to happen. And these workers are not going to find jobs that pay nearly as much, and they are the ones who have 401k accounts and make those contributions. Unhedged: So it’s not that AI is a bubble that bursts, it’s that AI works too well, sucks labour out of the system and then you have less money flowing into markets? This virtuous cycle that has powered the indices, and in particular, the AI stocks — that gets thrown into reverse hard. So the irony of this will be that, over the medium term, the companies whose stock prices have been the biggest beneficiaries of enthusiasm around AI will get hit among the hardest. So that’s when you get ka-boom. And that I believe creates a GFC-type scenario. It will spill over very quickly into credit, commodities etc.’

This isn’t a problem until it is. Something to keep in mind should the market roll over.

‘Margin debt is surging into territory that has some investors on edge, firmly in what many would call the danger zone. For now, however, margin debt expansion supports the momentum upside, but any reversal will also fuel the sell-off. It’s a double-edged sword that cuts the deepest on the downside.’

Credit Spreads Close to All-Time Tights

No problem accessing credit for investment grade issuers.

‘US credit spreads close to all-time lows. Despite higher yields and geopolitical turmoil, the credit market remains very sanguine. As a result, financial conditions remain very loose.’

Equity/Bond Yield Correlation at Low Levels

Stocks and bond yields moving in opposite directions is a powerful force. Correlations are, of course, unstable. Pay attention to government yields.

‘The stock-bond relationship is showing a rare pattern: The 2-month correlation between US equities and the 10-year Treasury yield is down to -0.70, the lowest since 1999. In other words, over the last 2 months, stocks and the 10-year Treasury yield have moved in opposite directions by the largest extent this century. At the start of 2026, a positive correlation of 0.40 was observed, near the highest since 2023. Additionally, the 30-day correlation is down to -0.68, also the lowest in 27 years. Not even the 2022 bear market saw such a negative correlation, as the 10-year yield rose, driven by elevated inflation and Fed rate hikes, while stocks fell. Bond markets are incredibly important right now.’

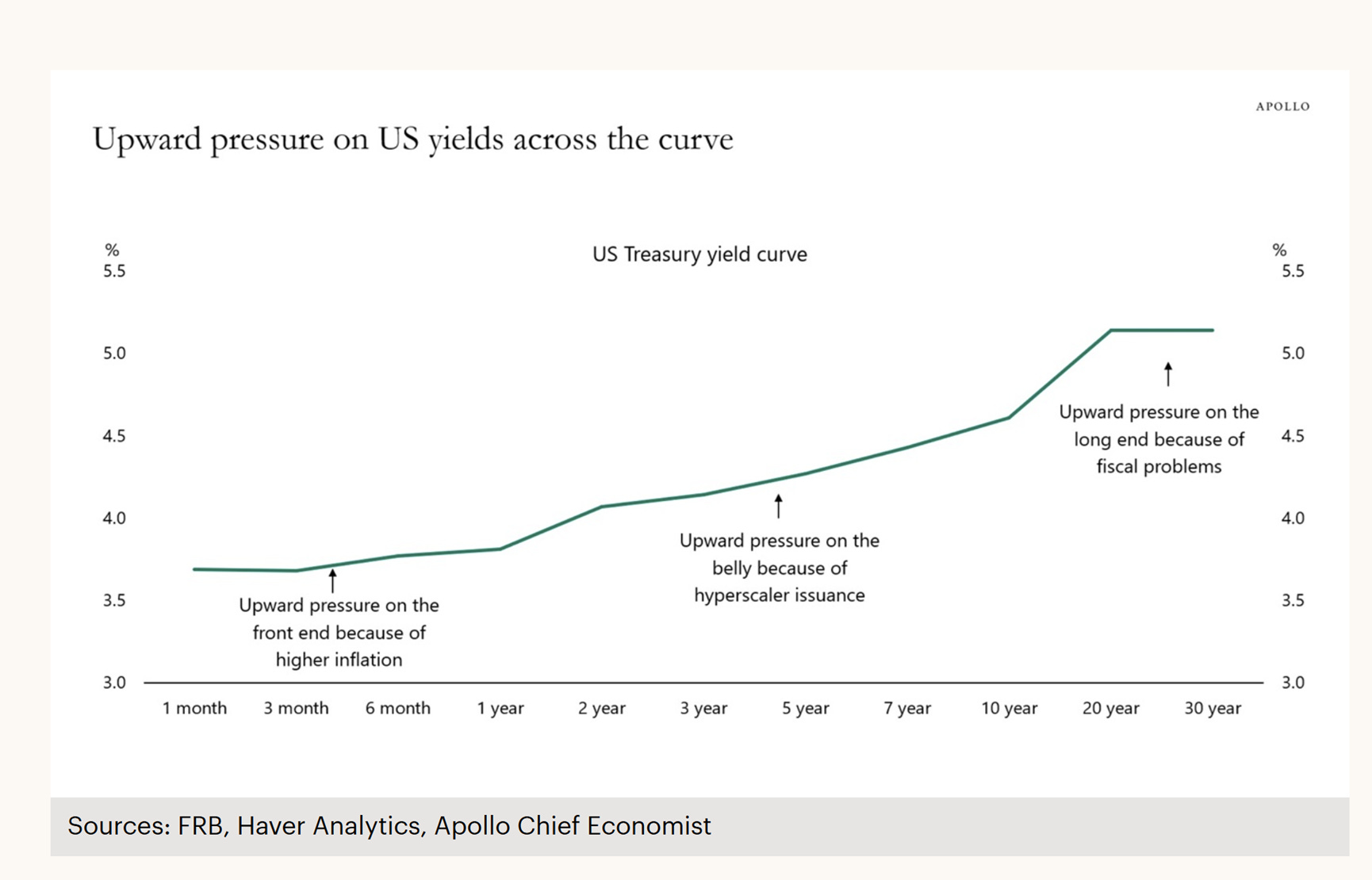

Rates Going Higher for Longer Driven by Three Independent Forces

Rates did nothing and then they moved. The natural reaction would be to think that the higher yields will attract interest and we’ll retreat back into the range. But this may fly in the face of three separate, powerful trends. They were there before, but now the market is attentive to them.

‘Front-end rates are under upward pressure because inflation is higher for longer.

‘The belly of the curve is seeing upward pressure on yields because of hyperscaler issuance.

‘And long-end rates are moving higher because of more Treasury supply and less Fed demand.

‘The bottom line is that three distinct forces are pushing rates higher across the curve, and investors should position for a persistently higher rate environment.’

Equity Issuance to Hit All-Time Highs

Companies selling stock on the highs.

‘The scariest thing in public markets right now... (chart from GS)’

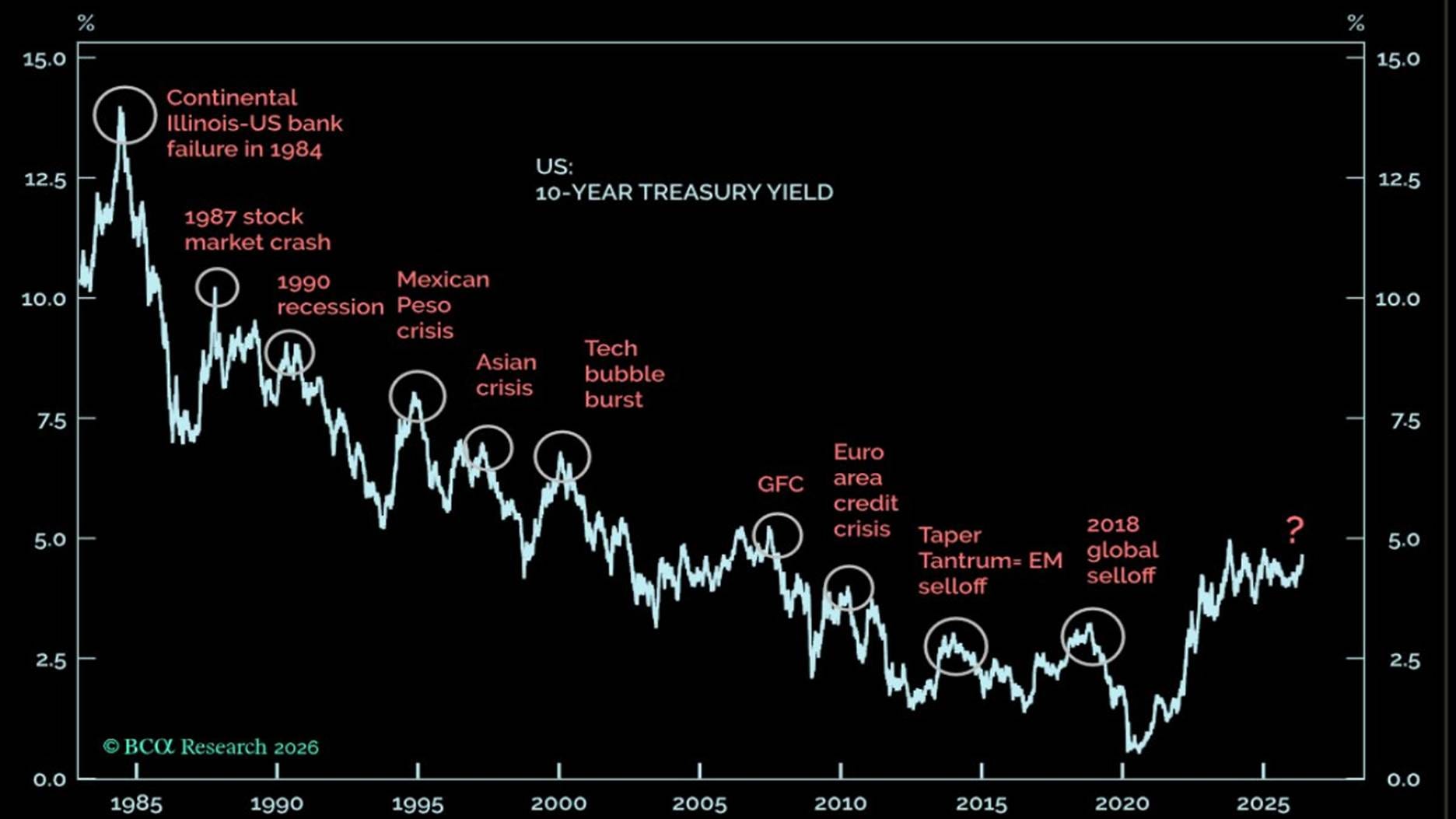

BCA: The Bond Market Is Key Here

Put this together with the negative correlation between equities and bond yields and the market is potentially very sensitive to yields.

‘BCA: “US bond bear markets always end with turmoil in stocks” https://zerohedge.com/the-market-ear/us-bond-bear-markets-always-end-turmoil-stocks’

Disclaimer: The content in this publication reflects my personal trading activities, market observations, and investment thought process. Nothing here constitutes investment advice, financial advice, trading advice, or any other sort of advice, and you should not treat any of this content as such. I am not a registered investment advisor or financial professional. All trading and investment decisions carry risk, including the potential loss of principal. You should conduct your own research, perform your own analysis, and consult with qualified financial professionals before making any investment decisions. Past performance does not guarantee future results. I may hold positions in securities discussed.