Point Frederick – Spinnaker – May 20, 2026

When rate volatility picks up, it's only natural to think about the risk to the plumbing.

Whenever there is rate volatility, we need to think about the next financial blow-up. The system is more brittle than people know.

Take, for example, Silicon Valley Bank: a regional bank with long duration assets funded by flakey short-term deposits. When rates increased, they endured a mark-to-market loss that was not apparent on the financial statements as these were held-to-maturity assets that didn’t require the same kind of mark as available-for-sale securities. It happened slowly, then quickly, but depositors ran for the hills. As it sold off its available-for-sale securities, the reality of the marks started to bite, held-to-maturity or not. Equity disappeared quickly.

Could we see some regional banks look shaky? Presumably the regulators are all on the lookout for this kind of risk. Nobody wants to get pantsed by plain vanilla risk again.

Many hedge funds are engaged in the basis trade: long cash Treasuries financed in the repo markets and short futures contracts financed at the futures-implied financing rate. You earn the futures-implied financing rate less the repo plus any expected pricing convergence over time. If the plumbing starts to shake, then anything can happen. Repo rates can increase. Funding sources in the repo market can cut back on the amount of permitted leverage, forcing you to either liquidate or pony up more cash. Given the scale of things, forced selling of cash Treasuries can push the basis wider, begetting more margin calls and restrictions on leverage, in a vicious cycle.

What would happen to dealer balance sheets? Could June month end be a catalyst?

That kind of fear and loathing isn’t good for risk.

And we wouldn’t know how this new Fed/Treasury partnership would respond.

The Standing Repo Facility caps repo rates in times of crisis. Would Warsh impose limits or restrictions on that? Would he follow up with QE given his comments on the size of the balance sheet? Even with the Standing Repo Facility, there is nothing to stop the banks from forcing hedge funds to deleverage.

What happens in asset-backed securities markets when rates back up? Holders are short convexity, so they need to sell Treasury hedges into the market. This contributes to the size of the directional move lower.

Could we have a UK-like rates/liquidity spiral in the US?

Chinese Commodity Stockpiles Are a Monetary Base

This is a fascinating theory.

China’s sitting on massive inventories of oil. They accumulated these stockpiles when Biden sold out the Strategic Petroleum Reserve for, ahem, reasons. They have massive stockpiles of other commodities.

US dollars are the script with which US citizens (human and corporate) pay taxes. We use them as fiat currency because what could be more solid than paying taxes.

The fact that Chinese inventories have not fallen since the commencement of the hostilities with Iran is being interpreted by some as proof of the genesis of a new non-dollar collateral system: script representing claims collateralized by those inventories. That’s why the inventories aren’t moving. They’re not being used as anything other than a backstop. There’s paper flying all over the place backed by claims on the inventory.

Think of it as a shadow dollar.

This means that China won’t be selling the commodities behind this script when prices spike and they’ll be the bid on the downside. Take that to its logical extension and the floor for commodities just got higher, even as the upside has moved up. They’ve smoothed the downside and they’ve opened up the possibility of spikes on the upside.

If Chinese stockpiling makes key commodities like oil behave more like monetary reserves than industrial inputs and most investor allocations to commodities are still low, then it makes sense to consider if you have enough direct and indirect exposure to commodities in your portfolio.

‘Below is a very long analysis that asserts that Chinese commodity stockpiles may be moonlighting as the monetary base underpinning a highly leveraged dollar-proxy liability system that operates largely outside the formal dollar-clearing architecture. The analysis was prompted by one very odd anomaly: despite widening regional supply disruptions and materially weaker imports, Chinese energy stockpiles still don’t appear to have been meaningfully drawn down at all. That sits rather awkwardly with the conventional explanation that these are simply straightforward strategic reserves being accumulated for emergencies.

’

Commodities Are Focused on Scarcity, Not Debasement Any More

It’s an interesting argument. The big bull move in precious metals was focused on debasement. The US dollar was going into the tank. Large organizations were going to pay for trade with Chinese Yuan, I suppose.

The war in Iran has highlighted the need for dollars. There’s a scramble for swap lines. The selling in gold is consistent with this theory, too. If this theory is true, then gold and silver and platinum and palladium, not so much.

‘When we are in an era of scarcity, dollars go towards commodities of need that are in short supply. Debasement assets like Gold don’t fit that bill here and I think that’s why it is going nowhere. Read more below.’

Reasons Investors Are Selling Government Bonds From UK to US

There are lots of reasons why and they’re all pointing in the same direction.

‘Put it all together and the average 10-year yield across the Group of Seven rich nations is the highest since 2004, according to Apollo Management’s Torsten Slok.’

Is Keynesian Policy Going to Continue in the US?

Bessent was part of the brain trust that broke the Bank of England. Will he be broken? He’s got a tricky position, but if we want to predict him, we need to understand him. To hunt the rabbit, you need to think like the rabbit.

Everyone assumes that we’ll use the same old playbook. Everything is a demand weakness, or so we’re told. What if the volatility suppression regime gives way to structural change?

‘Food for thought., Wall Street is pricing continuity. That looks misplaced. US Treasury secretary Bessent is not a conventional appointee. He is a former macro hedge fund manager, architect of one of the largest trades in modern markets, with deep roots in credit and a grounding in supply side economics. He has also taught the history of economic thought. This is not a Fed trained technocrat. Nor is he alone. A new Fed chair steeped in a similar intellectual framework reinforces the shift. For two decades, markets have operated within a Keynesian frame. Policy smoothed cycles, suppressed volatility and anchored expectations. That reflex is now embedded in pricing. It may no longer hold. A Treasury shaped by markets rather than models is less likely to prioritise stability over regime shift. Volatility becomes a feature, not a bug. Capital markets have not caught up. They are still positioned for calibration, not change. The game has moved. Investors expect policy steeped in Keynesian dogma, led by officials distant from markets. Instead, they face a Treasury that understands how markets function and may choose to use that understanding. Have a nice day.’

Equities Moving Down as Bond Yields Move Up

This is why we care so much about bond yields all of a sudden.

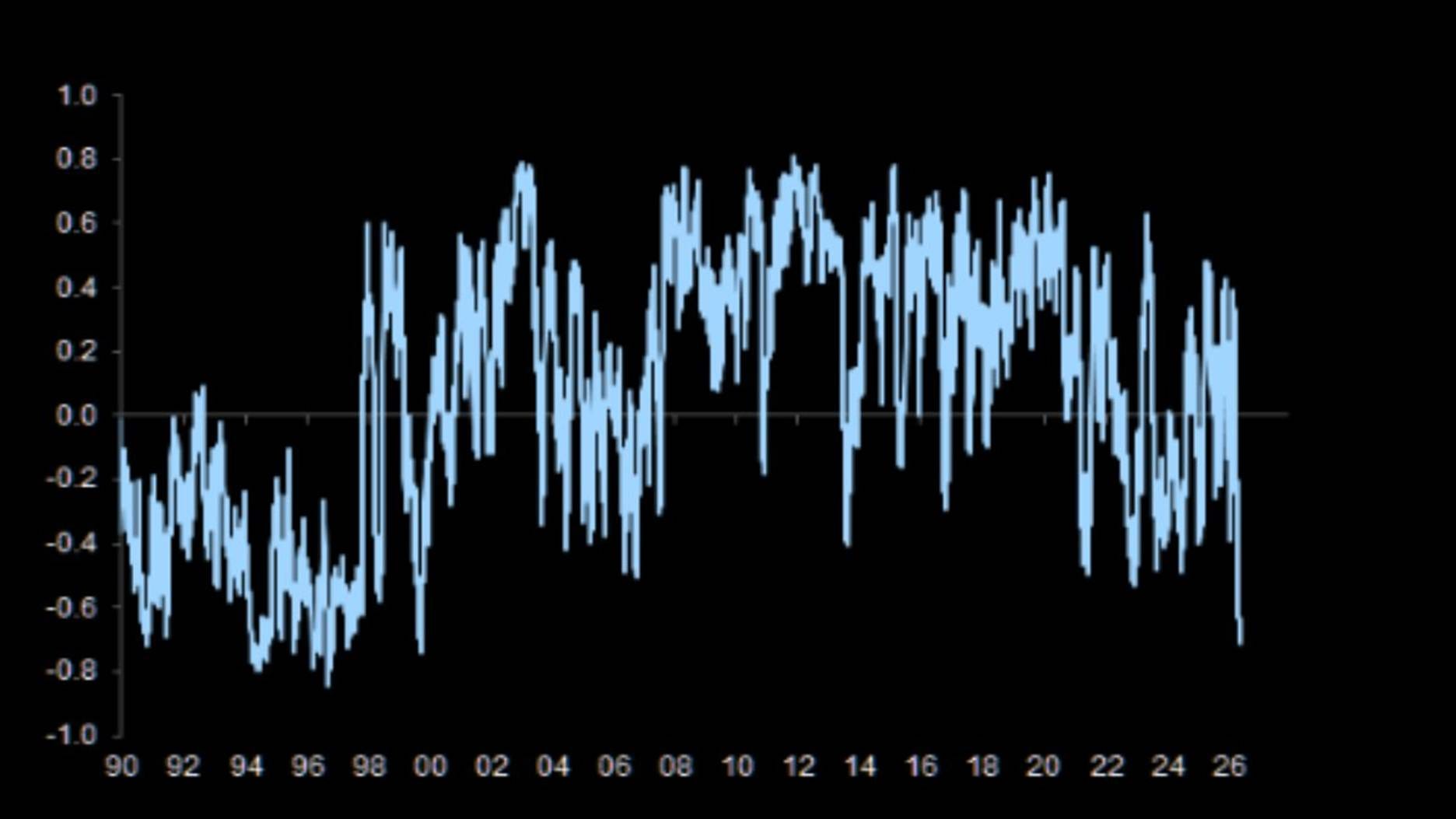

‘Equity/bond yield correlation has reached the most negative levels since the 1990s’

Investors warn of ‘correction’ risk as high-flying stocks defy bond gloom

It is amazing how fussy markets are. The regime shifts are coming in fast and furious. I wrote earlier this week that I was neurotic. Markets are neurotic right now.

‘“We will see a correction — the question is more when than if, in my opinion,” said Vincent Mortier, chief investment officer of Amundi. Mortier said that the equity market had “seen a total change of narratives, views and positioning in a matter of six weeks” in contrast to bond investors’ focus on the surge in prices for everything from diesel to petrol and jet fuel triggered by Iran’s closure of the Strait of Hormuz.’

Disclaimer: The content in this publication reflects my personal trading activities, market observations, and investment thought process. Nothing here constitutes investment advice, financial advice, trading advice, or any other sort of advice, and you should not treat any of this content as such. I am not a registered investment advisor or financial professional. All trading and investment decisions carry risk, including the potential loss of principal. You should conduct your own research, perform your own analysis, and consult with qualified financial professionals before making any investment decisions. Past performance does not guarantee future results. I may hold positions in securities discussed.