Point Frederick – Spinnaker – May 14, 2026

I don't think most people understand the exponential growth in AI and what it means for civilization.

The US Armed Forces administer an intelligence test to all recruits. There is a minimum threshold score they require for service, of course. But the broader use of the test is to assign individuals to a specific trade within the military, e.g., Infantry, Armored, Intelligence, Cyber, etc.

They have found over time that it’s best to have people work together who are within a band of something like twenty points on this specific IQ test. Beyond this level, say to have a 140 working with a 100, communication starts to break down. They don’t understand one another. It’s not just the 100 who can’t understand the 140. The 140 can’t understand the 100. It’s harder for them to get along.

There are people who succeed from every level.

There are generals and sergeants-major from practically every occupation, men and women with the highest decorations from every grouping.

I suspect that we see the same sort of IQ selection in civilian life. Birds of a feather flock together. People elect to go into a profession, say the law, in part, because they see the people who are lawyers already and can imagine fitting in with that crowd. There is a sorting that takes place that may not be as explicit or as directed as the ASVAB.

Just as in the military, one can obtain the heights of success in the markets regardless of background.

Being a Caltech quant is not a necessary condition for making money investing. It’s an open question if it’s sufficient.

You can be a fundamental investor with an undergraduate degree in philosophy and make money.

You can come from a humble background or a wealthy background. You can be an immigrant or a Mayflower descendant.

There are a million ways to make money. You can play special situations like spinoffs. You can buy the market index consistently. You can buy the names you like.

Every one of these methods involves paying attention, using your own judgment, and being disciplined.

We are in the early stages of a radical transformation of the way we live and the way our economy works. People are only now beginning to appreciate it.

I’m a self-taught coder. I learned AWS, a few coding languages, deep learning, and something about transformers before the revolution of the past twelve months. I did it the old fashioned way. I took courses. I read books. I programmed small projects. I debugged large projects that I had inherited. I fixed problems in a complex AWS deployment to the point that it could pass an Amazon technical review.

But I’m still blown away by the new AI tools.

Last year, I decided that I needed to redo the marketing website for a project I’m working on. When it comes to coding activities, this is pedestrian. It’s like riding a bike with training wheels.

Initially, I hired a web developer and gave him detailed instructions about what I wanted. It was a Wordpress instance. I thought that he would be better at the design part than me. I wanted to exploit his experience from working with other similar clients.

In the end, I didn’t like what he did.

I spoke with some friends about this and they whipped something up in an hour using Claude. This included setting up a database for the blog posts. They did this with no instructions from me. They intuited what I wanted in a way that the professional developer didn’t (or couldn’t).

It was wonderful. It is a sexy beast. The content needed to change, but it was perfect.

They then took the code and set up a repository in Github and hosted it in Google Firebase.

They had me clone the Github repo into my local machine and they gave me access to the Firebase instance.

But then they told me to use Claude Code to edit it. Coincidentally, I had just installed Claude Code and was about to start playing around with it.

After giving Claude access to the repo and to Firebase, to edit the words on the site, I just told Claude to change the specific text I wanted changed. In plain English. No commands. No HTML.

To replace the whole content, all I needed to do was to drop a PDF document with the new material into the prompt and say, “Use this content while maintaining the style of the current website.”

To deploy the new version to Firebase, I just typed, “Deploy.”

It did all the change work in the time it took me to make my coffee.

The first-order implication of this AI revolution is that you won’t need the same amount of people to do a base level of work, so there will be layoffs. The inefficient will get laid off.

The second-order implication of this is that people who get good at doing this can be one hundred times more productive than they would be otherwise. They can spawn armies of agents and subagents to do all kinds of work for them, just like Claude Code did the work for me. We are going to generate so many interesting applications that our biggest problem will be selecting amongst them.

The layoffs will come where there are inefficiencies. But the growth in hiring will come to exploit the new step-change higher in productivity.

If you see layoffs, it’s a signal that the company knows what they’re doing. It used to be a sign of weakness.

The third-order implication of this is that anyone will be able to do anything.

There is no reason the owner of a small HVAC company cannot do what I did with Claude Code and set up his own website. He doesn’t need to have some newly minted MBA buy him out. The secretary who has an idea for an application can make it happen. The costs of execution are plummeting.

The fourth-order implication of this is that everything is going to move faster.

Anyone who grew up expecting life to be slow and easy is now at risk.

The fifth-order implication of all this is that organizational structures will change. We can automate compliance, removing the role and power of the discretionary bureaucrat. Internal transactional costs will drop dramatically. Bureaucracy itself may become an unnecessary vestige of the industrial age.

It’s indescribable how quickly these AI tools are evolving. The growth is exponential as people build tools by using the most recent tools. Just wait until the tools build tools themselves.

If this thesis is correct, then you don’t own enough AI.

People are underestimating the implications of AI just as liquidity and the credit cycle are being very supportive of risk.

‘The current credit cycle melt-up is being driven by two things: 1) Financial market liquidity is expanding AT THE SAME TIME credit is being injected into the underlying economy. This creates a reflexive feedback loop between the market and economy as they feed on each other and risk assets are the release valve of this liquidity and credit. 2) AI is fundamentally retooling the market and economy in a manner that people don’t really understand yet. AI is speeding up the pace at which goods and services are transacted in the economy. It now costs a lot less to spin up a company, market it, and build a brand. This can happen with very little upfront capital which means that more businesses generate cash flow with less up front investment. On net this basically injects more cash into the system without being very capital intensive. The same thing is happening in financial markets with capital allocation decisions. The problem is that there is an increasing amount of money chasing the same amount of investments even though things in the economy and market are operating faster due to AI. I have been explaining all of these factors daily on the livestreams I do and in the daily reports i send out (both of which can be found on my website which is linked in my bio)’

Cisco Earnings Look Great and They’re Laying Off People

Normally, layoffs would cause the stock to sell off. It is meaningful that layoffs are cause for celebration.

‘Cisco jumps over +14% adding to its +32% gains YTD after a fourth-quarter sales forecast that exceeded analysts’ estimates and announced a restructuring that will eliminate around 4,000 jobs. Revenue will be $16.7 billion to $16.9 billion in the period, which runs through July, the company said. Adjusted earnings will be roughly $1.16 to $1.18 a share. Analysts estimated sales of $15.8 billion and profit of $1.07 a share, according to data compiled by Bloomberg. The company’s announced restructuring plan will allow it to invest more in AI and other growth opportunities the company said The move will result in as much as $1 billion in severance costs and other one-time expenses. The cuts will affect fewer than 4,000 jobs, or less than 5% of the total employee base, the company said.’

Hedge Funds Were Selling Tech Stocks

They sold …

‘MarketWatch: Goldman Sachs’ prime-brokerage division says that hedge funds may have been selling the rally in chip stocks. “Amid the group’s explosive price rally since the end of March (SOX +59% as of May 11th), US Semis & Semi Equip stocks collectively have been meaningfully ‘net sold’ by hedge funds based on Prime data (excluding options) during the same period, driven mainly by long sales,” said analysts led by Vincent Lin. Lin says managers may have used the rally to take profits while still playing for upside via options and other limited-loss formats. The firm does see “signs of chase and euphoria” in the volatility and ETF space. Lin also notes asset managers have been forced to buy AI stocks because they can’t afford to miss out on the gains.’

Hedge Funds Pile Back into Long Tech

They need ‘em.

‘Well that didn’t take too long. Hedge funds are back to being super duper irresponsibly long tech stocks. This while there’s a huge chase of $SPX calls and tech stock calls by other participants. Just about everybody’s long now in a few crowded trades. Should be fun.’

People want exposure. By people, I mean retail.

‘Risk appetite is skyrocketing: Assets under management (AUM) in US leveraged ETFs are up to a record $177 billion. Since the March bottom, total leveraged ETF AUM has surged +$45 billion. Tech-oriented ETFs account for the majority of total AUM, at ~69% This comes as technology AUM stands at $65 billion, followed by semiconductors at $32 billion, and the Magnificent 7 at $25 billion. Furthermore, leveraged ETF AUM linked to the S&P 500 is $24 billion. To put this into perspective, total leveraged ETF AUM was just ~$30 billion in 2020. Investors are piling into leveraged funds at a record pace.’

Vol Buyers Came In Aggressively at 1 PM Yesterday

They have to chase it as the underlying market goes higher or threatens to persist.

‘Vega frenzy you’ll never guess what happened yesterday at 1pm to reverse the market slide: biggest ever inflow into 3x levered semiconductor ETF, SOXL.’

The Market Is Much More Violent on the Upside than on the Downside

Will the leverage and the options exposure cause collapse?

‘The ratio of up-day realized volatility to down-day realized volatility on the Nasdaq 100 has surged to 10 times in May, the highest since 1986. This simply means the index is moving 10 TIMES more violently on up days than on down days, with up-day realized volatility at 28.2 versus just 2.8 on down days. Nobody owned enough upside exposure going into this rally, and now investors who were underweight or effectively short are being forced to purchase call options to catch up, driving extreme one-sided upside moves. This is the “Spot Up, Vol Up” dynamic in its most extreme form, where rising prices and rising volatility reinforce each other in a feedback loop that becomes increasingly UNSTABLE. The positioning underneath this rally is becoming dangerously unstable, with leverage and options exposure accumulating to levels that risk collapsing under their own weight. When almost nobody owns downside protection, and everyone is chasing upside, what comes next?’

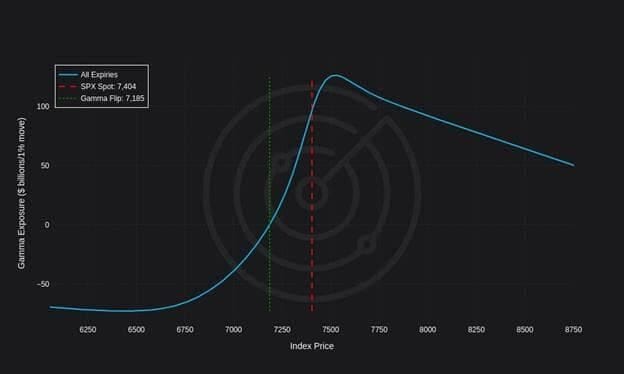

Gamma And Momentum: A Recipe For Cheers And Tears

ZeroHedge picks up a similar piece to our gamma squeeze comment from a few days ago and they follow through with discussion of the “gamma flip.” The implication of the chart below is that dealer gamma here stabilizes markets, but if we go back down through 7,185 on the S&P 500, gamma could cause some momentum lower.

‘When dealers are net short gamma (they have sold more options than they have bought), they are forced to buy stocks when prices rise and sell when prices fall to stay hedged. Thus, when dealers collectively hold short-gamma positions, they have to chase the market; their hedging activities amplify price movements and volatility.

‘On the other hand, when dealers are net long gamma, the opposite occurs. They buy weakness and sell strength. Accordingly, these hedging activities serve as a natural market stabilizer, dampening volatility.

‘The gamma flip occurs at the price level where a dealer’s gamma exposure crosses from positive to negative territory, or vice versa. This level is calculated by options analytics firms and is increasingly closely watched by institutional traders. The gamma flip is something of an invisible gravitational boundary in the market.

‘The graph below, courtesy of Radar Options, shows that as of May 11, 2026, the S&P 500 Index is in a long-gamma position, supportive of an uptrend with reduced volatility. If it were to flip negative by falling below 7185, we should expect increased pressure for further downside and higher volatility.’

The move in precious metals yesterday was bullish in their reaction to getting dumped on the open with the inflation news. They bounced hard.

‘And again: Algos dumped precious metals on hotter-than-expected inflation data. Then smart money stepped in and bought the dip once again. Silver now pushing toward $90/oz. Welcome to an unhinged inflationary era. Game on.

’

Despite the War, Energy Stocks Are Cheap

Energy stock are cheap vs the index.

‘Yet energy stocks, just like the rest of the market, have been reacting to every headline suggesting a potential breakthrough in negotiations between the U.S. and Iran. The price of the energy basket in the S&P 500 is just 2% higher than where it was before the war, when oil futures were close to $70 a barrel and the world had a supply glut. Today, oil prices are closer to $100 a barrel and the world has lost roughly a billion barrels of oil supply.

‘As a result, the sector that most directly benefits from the Strait of Hormuz closure has undergone the biggest earnings-multiple contraction since the start of the war. For investors lacking exposure to energy, this may be a good time to buy the dip.

‘True, the sector was trading at high multiples before the conflict began. Even so, the selloff in energy equities puts the group at less than 14 times forward earnings, making it 36% cheaper than the overall index. That is steeper than its 29% discount on average over the past decade. ‘

Disclaimer: The content in this publication reflects my personal trading activities, market observations, and investment thought process. Nothing here constitutes investment advice, financial advice, trading advice, or any other sort of advice, and you should not treat any of this content as such. I am not a registered investment advisor or financial professional. All trading and investment decisions carry risk, including the potential loss of principal. You should conduct your own research, perform your own analysis, and consult with qualified financial professionals before making any investment decisions. Past performance does not guarantee future results. I may hold positions in securities discussed.