Point Frederick – Spinnaker – May 13, 2026

We're all bond traders now.

We’re on a cuspy point right now. The biggest threat to the secular, explosive growth in technology names is the bond market.

Fiscal profligacy plus persistent, flaring inflation scares people. They’re nervous like the cat on the stove. It could be temporary, but after the last transitory fiction nobody’s going to play that game. The UK is the first one on the chopping block, but there are many other developed countries right behind them.

Any country that has weak growth, high leverage, poor investment, weak entrepreneurship, and political uncertainty is going to be in play.

I wouldn’t be surprised to see Korea overtake G7 countries shortly, if they haven’t done so already.

The volatility in the names that are part of the AI secular transformation will be something that longer term players are going to have to stomach.

Everybody’s a long-term investor until they aren’t.

There are no atheists in foxholes.

Live by the Bond, Die by the Bond

These days, when bonds go down, stocks go down. We’re facing some threshold levels that investors (and the Treasury Secretary) seem fixed on including 4.5% in the 10 year and 5.0% in the 30 year. In the recent past, these have held.

Also, keep in mind that the amount of hedge fund basis trading is at historically high levels. Will things start to break soon? Could this cause some funkiness in risk markets?

‘Stock / bond correlation the highest in nearly 20 years’

Help us, Scott. You’re our only hope.

It would have been glorious had the US termed out its debt structure when the yield curve was at its lows.

‘The US bond market crisis is intensifying. While everyone is focused on AI and the Iran War, the US bond market is in a complete meltdown. The 30Y Yield is now above 5.00% and the 10Y Yield is nearing the pivotal 4.50% level, which resulted in President Trump’s “90-day tariff pause” in April 2025. Long-term yields are now ABOVE levels seen prior to Fed rate cuts in another brutal reminder that the Fed can not contain the long-end of the yield curve. At the current pace, we will likely see US mortgage rates rise back above 7.00% this year. The question then becomes: How much longer can markets (or the US government) ignore the yield crisis? And, who folds first?’

Rosenberg Surprised by Bond Market Reaction to CPI

Same.

Is there something else happening beneath the surface?

‘The core CPI excluding the rental components (for which the BLS acknowledged a measurement quirk) came in at the oh-so-scary reading of +0.2% in April, which it has matched or been lower than in each of the past three months. During that time, this underlying measure of inflation has registered a +2.2% annual rate. I mean, for all the angst and anxiety over energy pass-through and tariffs, that’s all we get? Meanwhile, the bond market is having a mild coronary.’

The UK Gilt Market Is Vulnerable

Political uncertainty? Check. Feckless leadership? Check. Over-leverage? Check. The market worries that whoever replaces Starmer will be, ahem, further to the left. Good grief.

The problem with UK bond weakness is that it’s only a matter of time before investors start to bring this kind of fear to other developed fixed income markets. Anyone associated with Europe is going to be in a world of hurt. If you don’t have growth, then you’re on the back foot.

‘BREAKING: Top investors warn Britain faces a Liz Truss-style bond market revolt if Labour ousts Keir Starmer Michael Pfister, FX strategist at Commerzbank: “The goal of a balanced budget is likely to falter should a less fiscally conservative candidate take over. And in recent years, we have repeatedly seen situations where the British government bond markets came under pressure and the pound followed suit. This time, the situation is unlikely to be any different.” Cathal Kennedy, senior UK economist at RBC Capital Markets: “I think this morning there is a 2022 feel toward this, with the Prime Minister carrying on as normal while all indications show he has lost his authority in the party.” Craig Inches, head of rates and cash at Royal London Asset Management Ltd: “The market is now pricing almost four rate hikes for the UK which it can’t withstand. Whoever replaces Starmer will not be able to borrow more money via gilts regardless of what they say.” Mohit Kumar, chief economist and strategist for Europe at Jefferies: “Any replacement would likely be left-leaning and be negative for the long end of the curve and the currency. We maintain our steepeners and short position in sterling.” Jordan Rochester and Evelyne Gomez at Mizuho: “We’ve been looking for 10 year UK gilts to sell off towards 5.15% by year end for quite some time, but this political drama accelerates the timeline, and we could see a move toward 5.20% until the political situation is settled and/or 5.35% in extreme stress.” Laura Cooper, global investment strategist and head of macro credit at Nuveen: “Gilts are increasingly behaving like a real-time referendum on fiscal and political credibility, aggravated by the recent move higher in oil prices.” Roger Lee, head of equity strategy at Cavendish: “Even if Starmer resigns the political uncertainty is unlikely to end as internal rivalry within the Labour Party ramps up. To stabilize the gilt market the government may have to commit to the fiscal rules and the only candidate seemingly prepared to do that is Wes Streeting.” James Athey, fund manager at Marlborough Investment Management Ltd: “The last thing that Gilts needed was weakness in the US treasury market. Now we’ve got potential for the ceasefire to collapse, the US doing some fiscal expansion all on top of the utter domestic shambles that is UK politics.”’

The Trump Trade 2.0 is quite weird

The reactions to earnings are quite pronounced. You either have strong earnings or you don’t. And if you don’t, you will get savaged by Mr. Market.

‘What is clear is that earnings are crushing it (as Rob and I discussed on the pod the other day). Jim Reid at Deutsche Bank sums this up rather nicely here: Yowza. Citadel Securities points out some interesting stuff going on beneath the surface. One is that while the market is rewarding good earnings, it is seriously dunking on bad earnings. “Companies beating on both EPS and revenue are up +1.2% on average, versus -4.5% for those that missed,” it said. (See Whirlpool for details, as Rob wrote the other day.)’

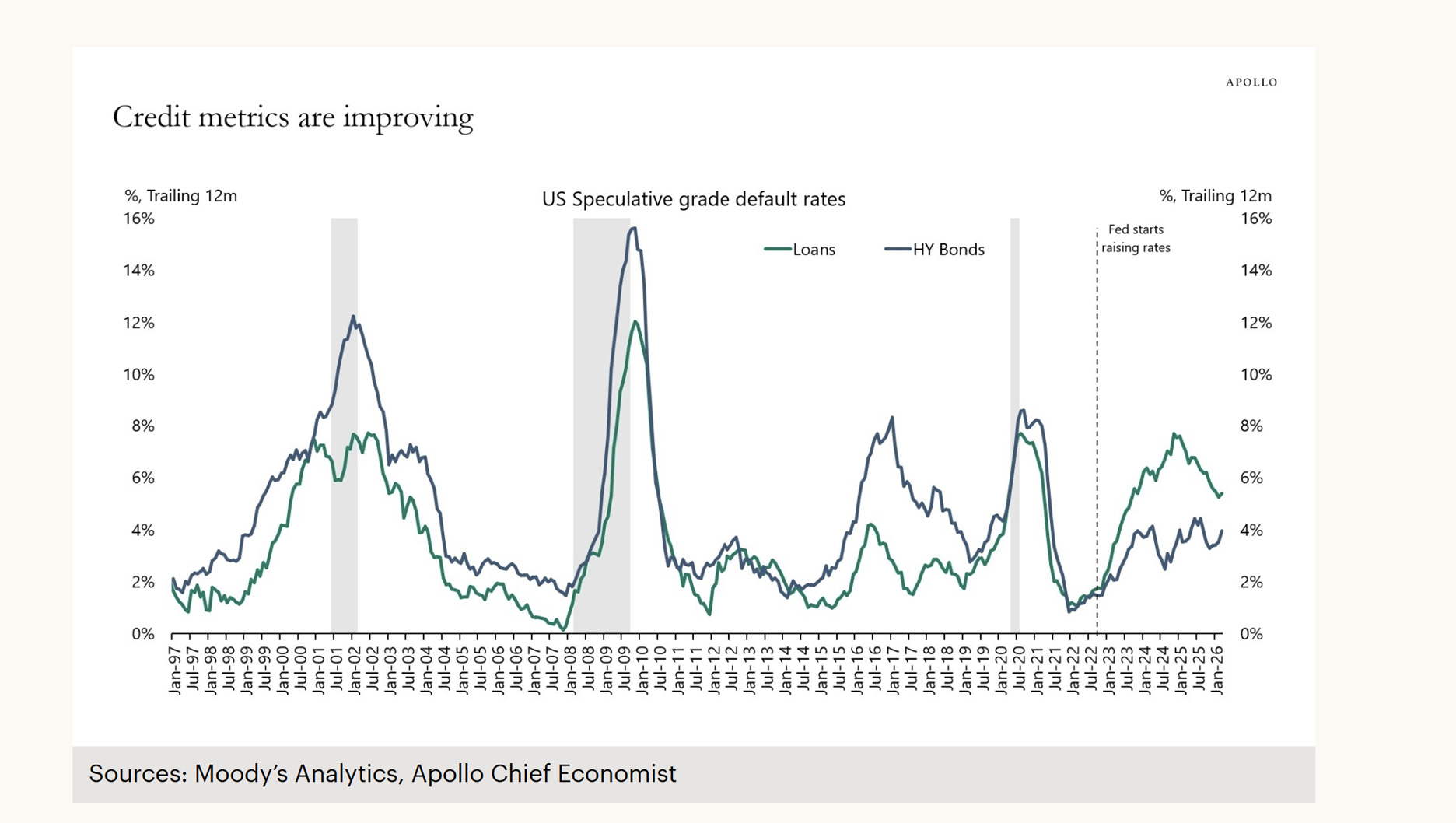

In Credit Markets, Things Are Getting Better, Not Worse

Credit metrics are improving. Has the bulk of the pig of covenant-lite lending passed through the python?

‘Default rates are falling, distressed exchanges are declining and the number of liability management exercises are declining, see charts below.

‘The bottom line is that the economy is strong and there are no signs of a full-blown credit cycle.’

We’re Still in the Midst of Unprecedented Technological Change

When things go up this much, as in technology like semis and Korea etc., people are keen to sell and protect their gains at the first sign of volatility.

We may just have to learn to live with it. You can sell on the choppiness, but you may not be able to get back in at reasonable levels, if only because of the psychological obstacles to doing so. How many people are detached enough to do this?

When you jump on the tiger’s back, you’d best hold on.

‘Food for thought., This is not a bubble. It is a repricing. A capital spending supercycle, full tax expensing through 2031, AI‑driven productivity, demographics and Trump’s America First industrial policy are structurally lifting the S&P 500’s earnings power. Hyperscalers are rebuilding the productive platform, the tax code pulls forward profits, and millennials are entering peak earning and investing years. Gold and memory have already been repriced as the world revalues scarcity and security; Bitcoin & equities are next. In that context, 8,000 in 2026, 10,000 in 2027 on $400 of earnings at 25 times, and 14,000 by 2031 look less like exuberance than arithmetic.’

BofA – Bubbles End When Bond Yields Surge Sharply

This is the principal risk, particularly when the market is focused on equities reliant upon cash flows showing up in the distant future.

Bessent knows he has a K-shaped economy.

He’s not going to go gently into that good night.

‘Thoughts from Michael Hartnett, BofA | Unusual macro regime Markets are entering a very unusual macro regime: strong stock markets, strong gold prices, resurging commodities/materials, and increasingly hawkish central banks at the same time. US equities and gold are both posting exceptionally strong multi-year gains simultaneously. Historically, that combination only happened during unusual macro periods such as wartime booms, bubbles, or stagflationary eras. The current environment mixes elements of: • AI/tech bubble dynamics, • geopolitical/resource competition, • inflationary/stagflation pressures, • and strong nominal GDP growth. Main bullish thesis: Major secular rotation toward: • materials, • commodities, • emerging markets, • and small/mid caps. Drivers include: • AI infrastructure CAPEX, • defense spending, • housing shortages, • resource nationalism/geopolitical competition, • and potential long-term RMB appreciation. • Materials stocks are only ~2% of S&P 500 market cap, near historic lows, which is an underowned sector with upside potential. • The “AI Big 10” now represent ~40% of S&P 500 market cap, similar to past historic concentration extremes (Nifty Fifty, Japan 1980s, dot-com era). • That does not necessarily mean an immediate crash, but it suggests bubble-like concentration risk. What could end the boom? • Historically, major bubbles tend to end when bond yields surge sharply. • Rising developed-market central bank hawkishness as a potential warning signal. Market positioning/flows: • Massive recent inflows into cash and investment-grade bonds suggest institutional investors are becoming more defensive. • Meanwhile, EM equities, China equities, and Europe equities recently saw notable outflows.’

Bloomberg – K-Shaped Wage Growth

Another reason why Bessent needs to be careful here.

‘Wage growth is increasingly concentrated among wealthier households. In April, higher-income households’ after-tax wage growth rose to 6% YoY, while lower-income households’ wage growth was 1.5% YoY, barely offsetting average increases in gas spending: Bank of America Institute’

American healthcare costs drive global imbalances

If the US really wanted to fix its trade imbalances, fixing its disastrous healthcare system is a wonderful place to start. The irony here is that you can get great healthcare in the US; it just costs an arm and a leg. The Obamacare fiasco made things worse. It would have been far more efficient to provide catastrophic insurance for the most vulnerable instead of trying to force feed a weird artist’s approximation of socialized medicine on anyone not covered by an employer plan.

‘But it might help to be clearer. If persistent surplus countries are under-consuming, persistent deficit countries are likely to be over-consuming. And what the biggest deficit country in the world is consuming at a massive scale is healthcare. At roughly 17 per cent of GDP, the US spends at least an “extra” 5 per cent of GDP on health care compared to some of its closest peers, but with worse outcomes in both coverage and results. Around 27mn Americans are uninsured, and average US maternal mortality rates across all groups are multiples of those seen in the UK or Germany.’

Disclaimer: The content in this publication reflects my personal trading activities, market observations, and investment thought process. Nothing here constitutes investment advice, financial advice, trading advice, or any other sort of advice, and you should not treat any of this content as such. I am not a registered investment advisor or financial professional. All trading and investment decisions carry risk, including the potential loss of principal. You should conduct your own research, perform your own analysis, and consult with qualified financial professionals before making any investment decisions. Past performance does not guarantee future results. I may hold positions in securities discussed.